Unlock Your Home’s Hidden Wealth & Lower Your Payments

Your Home = Your Financial Superpower

Rates dropped? Credit improved? Need cash?

Your home has likely gained significant value over the years. Refinancing allows you to reset your mortgage terms, lower your interest rate, and access up to 80% of your home equity in cash.

Whether your goal is to reduce monthly payments, consolidate debt, or fund major investments, refinancing puts your home’s value to work for you.

Lower Your Interest Rate

Take advantage of improved market rates or stronger credit.

Access Home Equity

Unlock cash for debt consolidation, renovations, or investments.

Simplify Your Finances

Combine multiple debts into one predictable mortgage payment.

How Mortgage Refinancing Works

Two Powerful Options

Rate & Term Refinance

Reset your mortgage to secure a lower rate or better terms, with no cash taken out.

Cash-Out Refinance

Access up to 80% of your home equity while refinancing your mortgage.

Toronto Example:

Home Value: $1,200,000

Outstanding Mortgage: $600,000

Available Equity: $600,000

80% Cash Access: $360,000

That’s over a third of a million dollars in accessible cash at mortgage rates.

Perfect Refinancing Scenarios

✅ Rate Optimization

Market rates dropped 1%+ since your last renewal

Credit score improved 100+ points

Switch from high-rate lender (alternative/private to bank)

Remove mortgage insurance (reached 20% equity)

💡 Wealth Building Strategies

Debt Consolidation (eliminate 19% credit cards with 6% mortgage)

Investment Property Down Payment (leverage equity for rentals)

Home Renovations (tax-free equity vs. high-interest loans)

Business Investment (often tax-deductible when used commercially)

Education Funding (children's university, professional development)

📊 Break-Even Analysis

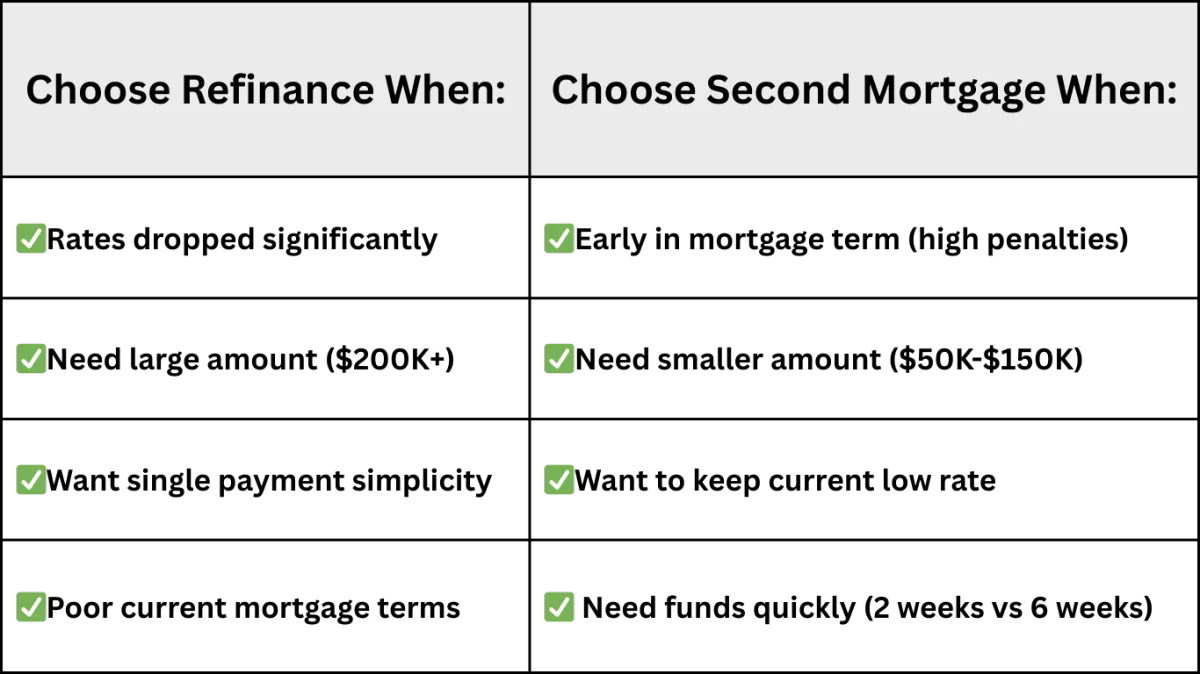

⚡ Refinance vs. Second Mortgage

When does refinancing make sense?

Refinancing makes sense when rates have dropped, your credit has improved, or when the long-term savings outweigh any early payout penalties.

How much equity can I access when refinancing?

Most homeowners can access up to 80% of their home’s value, depending on income, credit, and property type.

Are there penalties for refinancing?

Yes, some mortgages have early payout penalties. A break-even analysis helps determine if refinancing is still beneficial.

How long does refinancing take?

Most refinances are completed within 3–6 weeks, including appraisal and legal processing.

Can refinancing help with debt consolidation?

Yes. Refinancing is one of the most effective ways to eliminate high-interest credit card and personal loan debt.

What’s the difference between refinancing and a second mortgage?

Refinancing replaces your existing mortgage, while a second mortgage keeps it intact. The right option depends on penalties, timing, and cash needs.

“Refinancing changed everything for us.”

We had $85,000 in credit card debt at 22% interest costing us nearly $1,900 a month. Refinancing helped us pull out $100,000 at 6.2%, dropping our total payment to $650 a month.

We’ll be debt-free years sooner—and our home value increased another $180,000 since refinancing.

— Patricia & Tom W., Etobicoke

Your Path to Financial Freedom Starts Here

FSRA License #13564

BC License #MB605782

Stay Updated

Receive the latest mortgage insights and tips directly to your inbox.